17 May 2022, Boston, Massachusetts: The health risks and contamination associated with per- and polyfluoroalkyl substances (PFAS) are propelling state and federal legislators to crack down on the usage and spread of these “forever” chemicals impacting drinking water supplies. Boosted by an uptick in regulations and funding, drinking water remediation technology spend is forecasted at US$6.15 billion for this decade, according to a new report from Bluefield Research.

Total annual expenditure for PFAS treatment systems is estimated to scale from US$334.6 million in 2022 to US$1.1 billion in 2030. The state-by-state forecast in Bluefield’s report PFAS: Drinking Water Treatment, Regulations, and Remediation Forecasts, 2022–2030 is highly influenced by the extent of PFAS contamination within each state’s borders and the increasing adoption of state and federal policies.

“Without a doubt, PFAS has moved to the forefront of concerns for water utilities and the public at large,” says Lauren Balsamo, a Municipal Water Analyst for Bluefield Research. “This is the first time the federal government is expected to issue PFAS standards as well as dedicated funding to address remediation. At the same time, states continue to adopt their own stringent regulations.”

In only a few years, the U.S. Federal government has taken significant steps to research and address PFAS contamination across the nation, as outlined in the release of the Environmental Protection Agency’s (EPA) PFAS Strategic Roadmap in October of 2021. The EPA is now well underway in setting guidance on these chemicals, including implementing drinking water maximum contaminant levels (MCLs) by fall 2023. In addition, the recently legislated Infrastructure Investment and Jobs Act (IIJA), ushering in $55 billion of newly dedicated water sector investment, includes US$10 billion devoted specifically to addressing PFAS and other emerging contaminants.

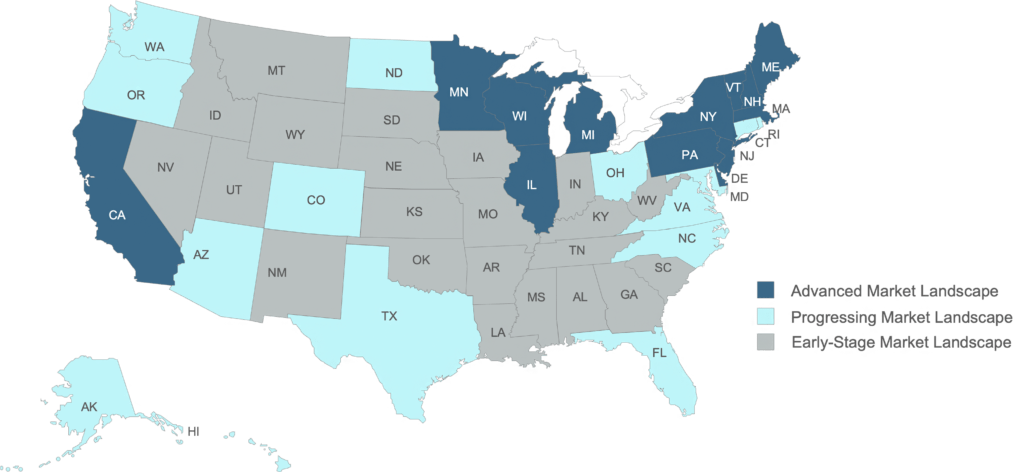

Exhibit: PFAS State Drinking Water Landscape Overview

Source: Bluefield Research

In the previous absence of federal guidance, highly affected U.S. states such as Michigan, New York, and New Jersey have already rolled out their own policies. To date, 44 states have legislated a range of policy mechanisms to limit PFAS contamination in drinking water. These efforts include drinking water maximum contaminant levels (MCLs), non-binding standards (i.e., health advisory levels), state mandated sampling of drinking water systems, and, at the very least, restrictions on firefighting foam.

California’s forecasted US$888 million of spend (highest of all states in the U.S.) is driven by the state’s high number of confirmed contamination sites, the state Water Board’s proactive testing for PFAS contamination, and a more rigid regulatory environment. At the same time, New Hampshire, despite its small size, falls into the top 20 spot for remediation spend at US$59 million, driven mostly by its more advanced regulatory landscape.

Some utilities, particularly smaller ones, may find themselves unable to navigate the financial, operational, and technological hurdles to meet the changing water quality requirements. “Public water systems, including investor-owned, will need to make significant investments to meet existing and impending standards,” says Ms. Balsamo. “Our team is keen to see if looming water quality standards will accelerate utility acquisitions, especially as smaller systems face additional financial pressures to address PFAS,” says Balsamo.