Available with corporate subscription

Market insight analyzing utility strategies to drive smart water meter adoption. Available for purchase and immediate download

European water utilities are deploying new strategies to become more efficient– taking steps to address non-revenue water and leakage management, while improving customer service. Smart meters are a critical first step– allowing utilities to harness the value of “Big Data” to manage unbilled water consumption and rising capital and operating costs.

This new Market Insight from Bluefield is essential for companies evaluating investment needs, outlook, opportunities, and trends in smart water across Europe. Topics covered include:

- Market Drivers & Inhibitors for Smart Meter Deployment

- Utility and Vendor Metering Strategies

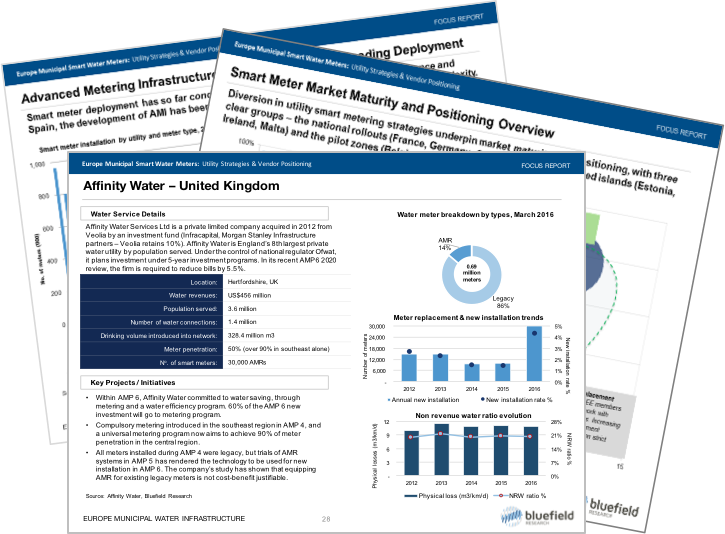

- Profiles of the 40 largest municipal utilities

- Profiles of the leading smart water meter vendors

Follow this link to access the Table of Contents

Click here for sample slides

Key questions addressed:

- What is the size of the European smart water meter market and what is the addressable opportunity?

- Where are metering rollouts expected to take place by country and by utility?

- What are the most successful utility strategies for driving the adoption of smart water metering?

- Which vendors are best-positioned in terms of utility wallet share and value chain?

- How will EU directives and national water policies impact smart meter spend over the next decade?

Special pricing available this week. Contact us to learn more.

Report Features

- 80-slide Market Insight (PDF)

- Bottom-up utility data (Excel)

- Bottom-up utility meter installed base, including analysis and vendor market share

- Smart water meter order book data and analysis by vendor

- Strategic analysis of smart water meter investment drivers

- +40 utility company profiles including meter breakdown, installation trends, non-revenue water ratios

- Profiles of leading meter vendors including value chain positioning, M&A, and key contracts