20 December 2022, Boston, Massachusetts: The municipal water sector in the U.S. and Canada is undergoing a transformation—from supply chain volatility and labor force disruptions to unprecedented infrastructure investment. These countervailing forces, among others, are reshaping the long-term trajectory and focus of US$1.8 trillion of capital and operating expenditures through 2030.

According to a new Bluefield Research report, U.S. & Canada Municipal Water Outlook: Utility CAPEX & OPEX Forecasts, 2022–2030, annual spend for approximately 70,000 water and wastewater utilities is forecasted to grow from US$188 billion in 2022 to US$223 billion in 2030.

While tracking a historical growth rate of 2.2% in Bluefield’s base-case scenario, the near-to-medium-term outlook remains tentative. Continued inflationary impacts on hardware, equipment, and labor prices and overarching concerns about potential recession loom large over an industry that only recently returned to pre-Great Recession spending levels.

“A renewed focus on utility infrastructure investment has gained momentum in recent years, particularly in the wake of the COVID-19 pandemic and growing concerns about water quality and climate resiliency”, says Bluefield’s Senior Research Director, Eric Bindler. “At the same time, surging material and equipment prices, unforeseen by utilities and vendors, are disrupting procurement decisions. Key input prices are up—for example, 134% for plastic pipes and 42% for treatment chemicals—since 2020” says Bindler. High material prices can push up costs for both capital projects and day-to-day operations and maintenance.

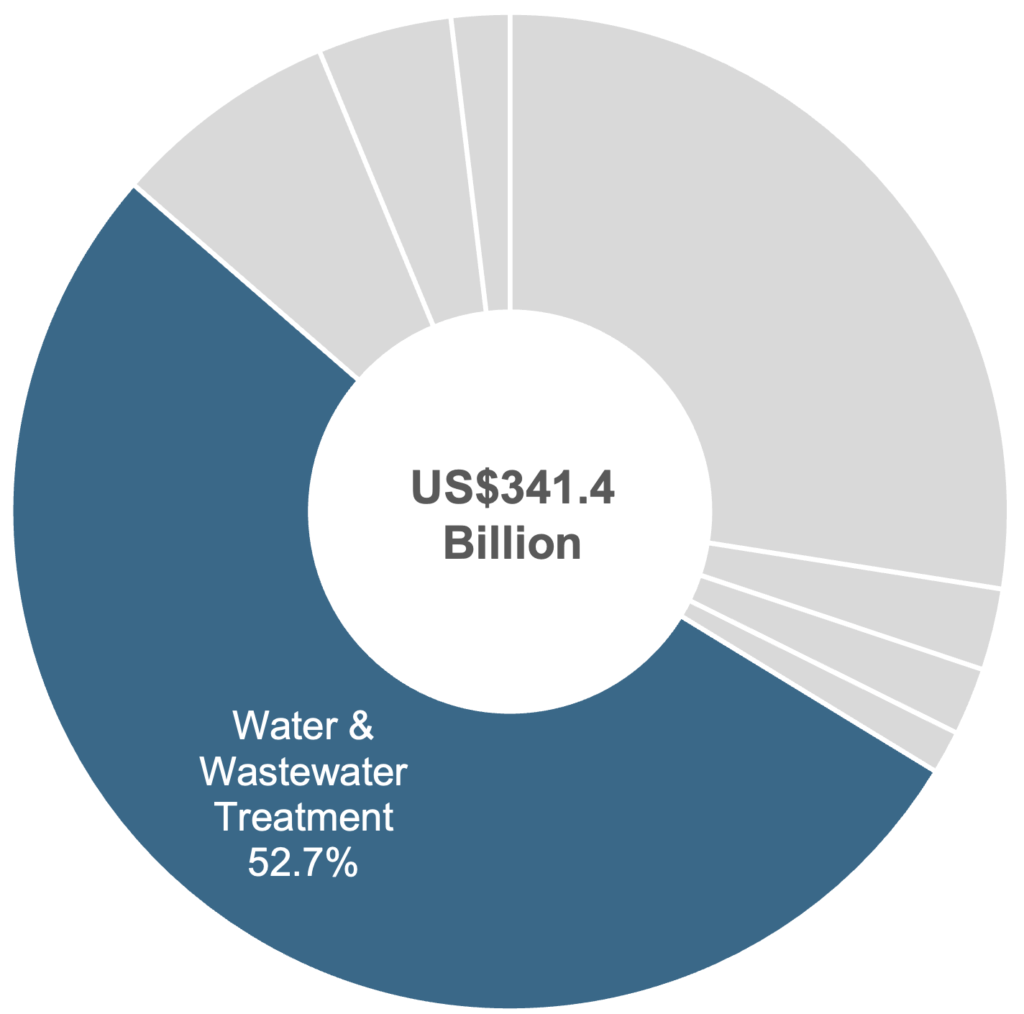

U.S. and Canada CAPEX by Asset Type, 2022—2030

Source: Bluefield Research

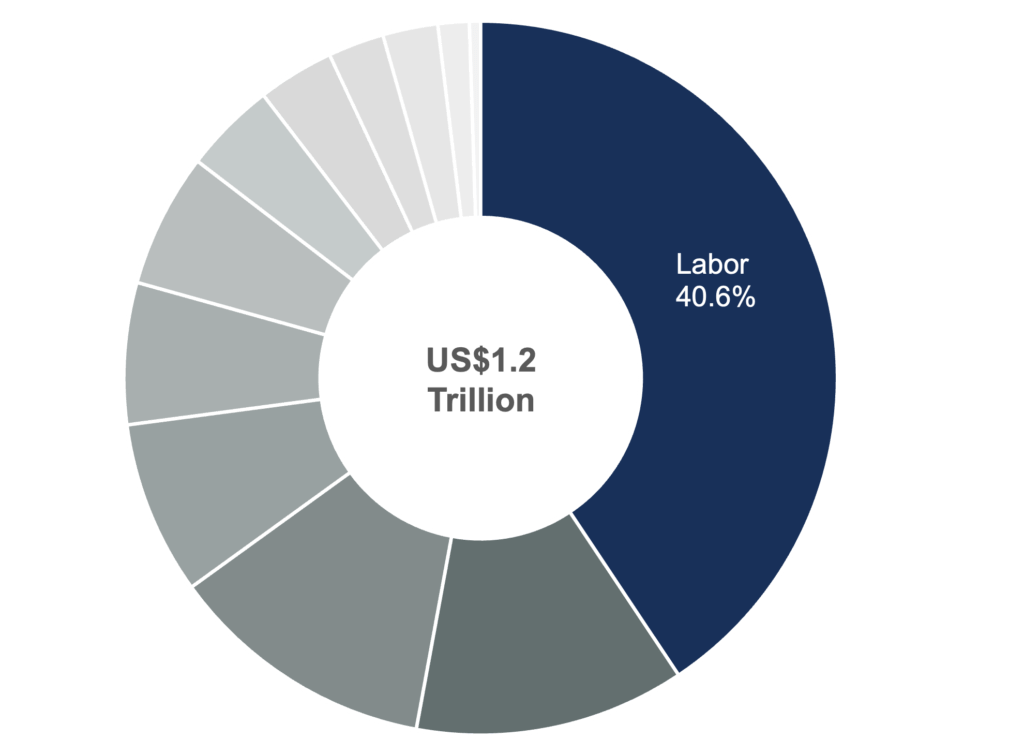

U.S. and Canada OPEX by Budget Category, 2022—2030

Source: Bluefield Research

Capital expenditures (CAPEX) for vertical assets (e.g., treatment plants, pump & lift stations, storage tanks) represent two thirds of total capital investment in the sector. Currently, spending on water & wastewater treatment plants, alone, is projected to total US$341 billion during the forecast period, which makes up 52.7% of overall CAPEX. This compares to US$218 billion forecasted for distribution and collection networks, including pipes, manholes, and valves.

Operating expenditures (OPEX), which includes ongoing labor, energy, chemicals, and maintenance costs, make up the remaining two thirds of projected total water utility spend. Labor costs are by far the biggest operating expense for water and wastewater utilities, accounting for a combined US$484 billion, or 40.6% of total OPEX. Employee recruitment, retention, and retirement challenges have been exacerbated by COVID-related attrition. Other factors influencing the forecasts include utility type (water, wastewater), size, region, and geography.

Following a decade of strong housing market growth and urban revitalization, water and wastewater utility demand is now being impacted by rising interest rates (i.e., mortgage rates) and an exodus of residents and workers toward more suburban and rural communities. As the former slows investment in new treatment capacity and pipe network additions, the latter can slice utility revenues, as demand for water and wastewater services pivots toward residential communities. This is particularly challenging for large, urban environments, like New York, Boston, and San Francisco.

Geographically, the most populous states and provinces— California, Texas, Florida, Ontario, Quebec—make up the lion’s share (32.2%) of forecasted CAPEX and OPEX. Meanwhile, population and housing market growth in hotspots like Utah and Alberta are driving more rapid market expansion.

“In terms of what to watch, the Infrastructure Investment and Jobs Act, or IIJA, may be one of the biggest factors influencing water utility spend over the next five years,” says Bindler. “With US$55 billion of new spend allocated for water and wastewater infrastructure through 2026, the scale and speed of the rollout will be influenced by stricter domestic sourcing requirements for equipment and hardware and new project prioritization requirements, such as an emphasis on disadvantaged communities.”