4 May 2026, Barcelona, Spain: Europe’s stormwater infrastructure is at a breaking point. Decades of underinvestment, accelerating climate risk, and expanding urban development have transformed a routine municipal function into one of the continent’s most pressing fiscal challenges, with flood damages now averaging €22 billion a year and rising.

According to a new report from Bluefield Research, Europe Stormwater Infrastructure Market: Key Drivers, Competitive Shifts & Investment Outlook, 2026–2036, total stormwater spending across Europe is projected to reach €643 billion through 2036, growing at a steady 1.7% annually. Yet this figure reflects only what cities are likely to spend, not what the infrastructure actually requires.

A Market Defined by Structural Underinvestment

With no dedicated stormwater fees or national budget lines in most markets, current investment levels run nearly 70% below what is needed to maintain basic service levels. Investment more often becomes available only after disaster forces the need: Valencia issued €3.76 billion in emergency tenders following a single flood; Slovenia mobilized €7 billion in reconstruction after 2023 floods wiped out 16% of its gross domestic product (GDP). Since 1980, flood damage across Europe has exceeded €385 billion, and precipitation data signals that the risk of larger, more capital-intensive storm events is only growing.

The scale of reactive spending points to a deeper structural problem. The European Commission’s Water Resilience Strategy estimates an annual investment shortfall of €23 billion, and nature-based and hybrid interventions consistently return €2 to €14 for every euro invested. Yet most governments default to emergency repair over prevention, compounding costs with every event they fail to anticipate.

“European stormwater systems were designed for a climate that no longer exists,” says Antonio del Olmo, a senior analyst at Bluefield Research. “The last three decades rank among the most flood-intensive in 500 years, and for cities, this is a crisis. For the companies building, repairing, and rehabilitating the infrastructure, it is one of the most compelling opportunities in European water management.”

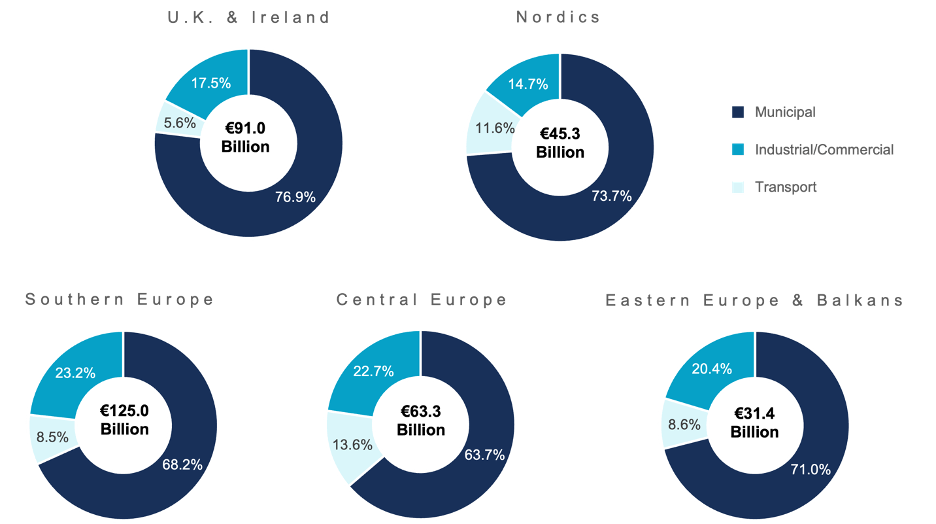

Exhibit: Stormwater Spend by Region, 2026–2036

Source: Bluefield Research

An Unevenly Distributed Opportunity

Europe’s stormwater market is not one market but several, each with distinct investment drivers, procurement dynamics, and competitive entry points. Western Europe, led by France (€92.9 billion), the United Kingdom (€85.2 billion), and Germany (€73.9 billion), accounts for the largest share of cumulative capital expenditures (CAPEX) through 2036, driven by mature regulatory frameworks and decades of deferred asset replacement now coming due. Eastern Europe and the Balkans, while representing just €31.4 billion in absolute spend, offer the steepest growth trajectory, as EU cohesion funding and Green Deal compliance drive investment in markets building modern stormwater infrastructure largely from scratch.

The route to that spending differs as sharply as the opportunity itself. Procurement models, decision makers, and competitive gatekeepers vary fundamentally across the continent such that a strategy built for one region is not applicable in another. Engineering consultancies, vertically integrated concessionaires, and EU-funded construction programs each control the market in different geographies, on different terms, through entirely different relationships. For companies seeking to compete across multiple regions, that fragmentation is the defining strategic challenge.

“There is no universal playbook for this market,” says Del Olmo. “The companies that will win are the ones that understand which door to knock on in each geography and have the relationships and credentials to get through it.”

As Investment Grows, So Does Competition

Conveyance and storage, the traditional backbone of stormwater infrastructure, are becoming increasingly commoditized. The new frontier is combined sewer overflow treatment, advanced filtration, and digital integration—segments where regulatory pressure is forcing utilities to go beyond their existing asset base and no single player has yet established a dominant position.

The competitive landscape today reflects that transition is in progress. Specialized mid-sized manufacturers—ACO Group, Hydro International, Hauraton, and BIRCO—compete on product performance and regulatory compliance, defending strong niches that national standards fragmentation has made difficult to displace. Large, diversified players—Suez, Veolia, Arcadis, Arup, Ramboll, Sweco, and Haskoning—engage stormwater opportunistically within broader water and infrastructure portfolios, but their role in design and specification gives them disproportionate influence over which products and technologies get selected downstream.

At the digital frontier, the competitive dynamic is shifting fastest. Established hydraulic modeling platforms—Autodesk (InfoWorks ICM), Bentley (OpenFlows), and DHI (MIKE+)—are facing a new wave of cloud-native competitors targeting real-time network management and predictive operations. Firms that secure embedded positions in municipal procurement specifications early will benefit from high switching costs and long adoption cycles, making the race for digital positioning as strategically consequential as any physical infrastructure contract.

For engineering firms, equipment manufacturers, and investors active in European water infrastructure, stormwater is no longer a peripheral opportunity within broader water portfolios. It represents a long-term, structurally driven growth market shaped by regulation, climate risk, and urban expansion.

“This market is being built by necessity,” says Del Olmo. “Climate events are accelerating timelines, regulations are hardening investment obligations, and the competitive positions being established today will be very difficult to displace once the spending scales. The window to get ahead of this is open now.”

About Bluefield Research

Bluefield Research supports strategic decision-makers with actionable water market intelligence and data in the global municipal and industrial sectors. With expertise spanning infrastructure, policy, and technology, Bluefield helps companies understand where the market is going—and why.

The Insight Report titled Europe Stormwater Infrastructure Market: Key Drivers, Competitive Shifts & Investment Outlook, 2026–2036 provides a comprehensive analysis of the European stormwater infrastructure market, including market drivers, regulatory dynamics, infrastructure forecasts, country case studies, go-to-market strategies, and profiles of 60+ companies active across the stormwater value chain. The full report is available for purchase and can be downloaded immediately from Bluefield’s website.