26 February 2026, Berkeley, California – U.S. agriculture is undergoing an US$84 billion water management transition, with farmers increasingly adopting more advanced precision irrigation systems to cope with declining aquifer levels, volatile weather patterns, and rising energy costs. This shift is fundamentally changing how farms allocate capital across irrigation equipment, water infrastructure, and digital technologies.

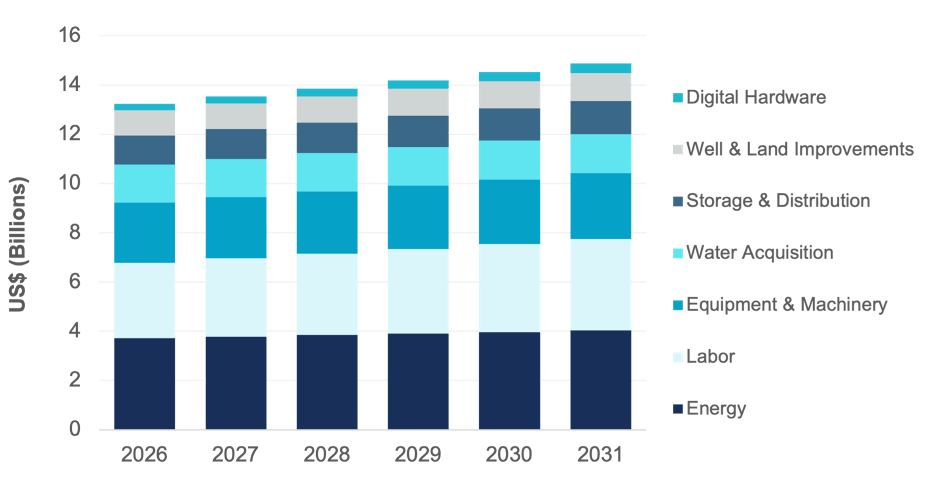

A new report from Bluefield Research, titled U.S. Water for Agriculture: Irrigation Trends, Technology Adoption, and Market Forecasts, 2026–2031, forecasts that U.S. irrigation spending will average US$13.5 billion annually over the next five years, split between on-farm irrigation systems and off-farm water delivery operations.

Agriculture accounts for roughly 70% of U.S. aquifer withdrawals, highlighting irrigation’s central role in both farm economics and national water security. “To address water scarcity, farmers are directing more capital toward drip systems and precision tools that reduce water usage while maintaining yields,” says Bluefield analyst Olivia Kranefuss. “For equipment vendors, timing matters. Once farmers commit to a system, they’re locked in for 10-plus years.”

Irrigation Market Splits into Two Distinct Buyer Groups

Bluefield has segmented the U.S. irrigation market into two distinct categories: on-farm and off-farm water management. On-farm water, pumped directly from groundwater wells, streams, and storage ponds by individual farmers, accounts for three-quarters of irrigation water usage and 77% of total spending.

Off-farm water is delivered through a network of roughly 850 irrigation districts, federal water projects, and private companies that manage canals, pipelines, and distribution systems. These off-farm organizations form a distinct infrastructure market characterized by larger capital budgets and longer project cycles.

This divide is most pronounced in Western states, where off-farm delivery supplies 51% of irrigation water—more than double the national average. This situation drives infrastructure investment in places like California and Texas, where water scarcity and federal grants are accelerating upgrade projects.

“Vendor approaches also differ by category,” Kranefuss notes. “On-farm sales rely heavily on dealer networks and financing to reach thousands of individual farmers, whereas off-farm infrastructure requires direct relationships with irrigation districts that control larger capital budgets and operate on multiyear planning cycles.”

Energy and Labor Costs Push Technology Adoption

Water scarcity is intensifying irrigation costs. Declining aquifer levels require deeper pumping, leading to higher energy use—which accounts for 28% of irrigation spending—and increased labor for system monitoring and maintenance. Together, energy and labor comprise 82% of irrigation operating expenses. These pressures are accelerating the adoption of water-efficient technologies, including variable-frequency drive pumps, automated controls, drip systems, and soil moisture sensors, which reduce water use while also lowering energy and labor costs.

“Pumping costs are the single largest expense in irrigation, which is a key reason we’re seeing accelerated adoption of efficient pump technologies and digital controls that address both energy consumption and labor intensity simultaneously,” says Kranefuss.

Exhibit Title: U.S. Irrigation Water Market Outlook and Growth Rate, 2026–2031

Source: Bluefield Research

Digital Water Technologies Lead Market Growth

Digital irrigation technologies represent the fastest-growing segment of the market, with spending projected to rise at a compound annual growth rate of 12.9% through 2031—more than double the overall market growth rate. This growth spans both hardware and software investments as operators seek to simultaneously reduce water consumption, cut energy costs, and address labor constraints.

Investment in digital hardware (e.g., soil moisture sensors, automated valves, variable-frequency drive systems, and remote monitoring devices) and software (e.g., irrigation scheduling platforms, cloud-based control systems) is expanding fast. Together, these technologies address the critical operating expenses by optimizing when to irrigate, reducing pump runtime, and eliminating manual field adjustments.

“The digital irrigation market is attracting capital from multiple directions—established manufacturers, agtech ventures, and precision agriculture platforms,” Kranefuss adds. “This investment wave reflects growing recognition that water management is becoming as data-driven as other aspects of modern farming.”

Competition Intensifies in Specialist-Dominated Market

The U.S. irrigation market is dominated by specialists like Valmont, Lindsay, Netafim, Rivulis, Jain, and Rain Bird, whose revenues are closely tied to farm water use.

Manufacturers focused on drip irrigation, such as Netafim and Rivulis, are gaining an edge over sprinkler vendors due to steadier demand driven by water scarcity and system conversions. Agtech start-ups such as CropX, Arable, and CeresAI are carving out positions with specialized sensors and software that compete directly with established vendors’ digital platforms. Leading manufacturers are increasingly offering bundled hardware with software subscriptions and flexible financing options—moves designed to lock in customer relationships and smooth cyclical revenues.

“Water scarcity isn’t a temporary challenge—it’s the new operating reality for U.S. agriculture,” says Kranefuss. “That permanence is driving sustained infrastructure investment and technology adoption that will reshape the irrigation landscape.”

About Bluefield Research

Bluefield Research supports strategic decision–makers with actionable water market intelligence and data in the global industrial and municipal sectors. With expertise spanning infrastructure, policy, and technology, Bluefield helps companies understand where the market is going—and why.

This Insight Report, titled U.S. Water for Agriculture: Irrigation Trends, Technology Adoption, and Market Forecasts, 2026–2031, presents a comprehensive analysis of the U.S. irrigation market. It encompasses market drivers, forecasts, regional dynamics, and the strategies of leading companies that are influencing the future of irrigation water management. The full report is available for purchase and immediate download on Bluefield’s website.