Boston, Massachusetts: Amidst increased demand for digital solutions from water utilities and industrial firms, a host of telecommunications companies are responding with dedicated strategies to capitalize on the burgeoning market opportunity, according to a new report from Bluefield Research, Connecting Water Infrastructure: Telecom Company Strategies in the Global Digital Water Market.

Digital water, which is the application of digital solutions and tools (e.g., hardware, software) for utility and industrial water management, has seen a 53% increase in project activity since 2016. Digital water spend in the top ten key markets is forecasted to grow from US$8.7 billion to US$20.2 billion by the end of the decade. Globally, this activity puts the growing sector on a 10% per year pace, led by the U.S., Australia, the U.K., and select Northern European countries.

In conjunction with the water sector’s growing appetite for more advanced communications, the industry’s unique and highly variable connectivity requirements are becoming more apparent. Communications network operators and vendors are targeting a range of data-related challenges that include power consumption, bandwidth, and cost.

“Telecom companies are by default well-positioned to meet growing demand for digital water connectivity within their existing geographies, capable of leveraging existing network infrastructure and local relationships,” says Nina Rossiter, digital water analyst from Bluefield Research. “When utilities and municipalities are looking for ways to connect assets and move data, telecom providers are often seen as a natural fit.”

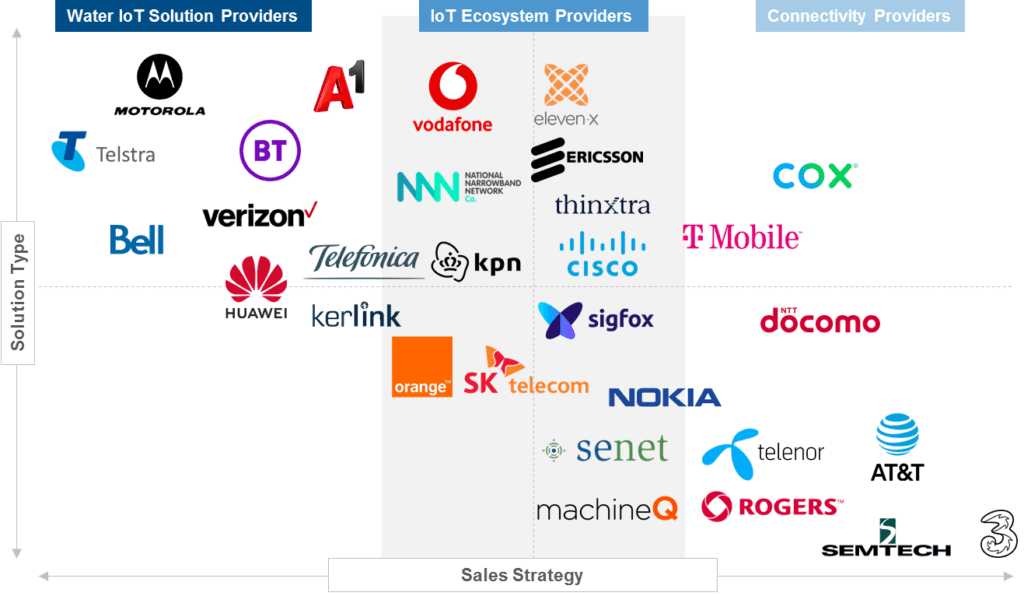

Exhibit: Telecom Firms’ Digital Water Strategic Positioning

Source: Bluefield Research

No longer content to serve as silent partners and indirect connectivity providers, select telecom companies such as AT&T, Vodafone, BT, and Huawei are carving out distinct strategic positions in water including go-to-market strategies and network offerings. Analysis of telecom companies globally, shows that select firms are vertically integrating their approaches by offering implementation and integration services. In some instances, like Telstra and Verizon, they are going a step further by selling proprietary hardware and software directly to water utilities.

These strategic pivots toward water are driving competition between established cell carriers, IoT network pure-plays, and water technology incumbents (e.g., water meter vendors). While the competitive landscape remains unsettled, the dynamics are further complicated by the emergence of new communications protocols (e.g., 5G, NB-IoT, and LoRaWAN) that are expected to accelerate digital technology adoption in water.

“In recent years, we have definitely seen an uptick in ‘outsiders’ looking into water from Big Tech to critical infrastructure players,” adds Rossiter. “Like these companies, telecom firms are more accustomed to different industry conditions, highlighted by faster sales cycles and technology adoption. How they respond to the fragmented and unique challenges of the water sector remains to be seen.”