BOSTON – Private participation in U.S. municipal water markets is poised for expansion, according to a new report from Bluefield Research. Municipalities and local authorities are showing an increasing reliance on investor-owned utilities and private players for the ownership, management, and operations of public water and wastewater systems. This market shift comes amidst a growing water infrastructure investment gap exceeding US$532 billion over the next decade.

“Municipalities are approaching a breaking point as utility assets reach the end of their useful lives. They must now seek-out alternative solutions for funding and technical expertise,” says Keith Hays, Vice President of Bluefield Research.

“Federal funding for municipal water has declined steadily in the past 40 years to barely 4%, leaving municipalities to finance infrastructure projects locally,” adds Hays. A more attractive regulatory landscape in key states is shaping new opportunities for companies looking to invest strategically in U.S. water. The lion’s share of investment activity will be focused on New Jersey, California and Pennsylvania, but increased M&A activity in Illinois, North Carolina, and Virginia highlights a transition toward new markets for growth.

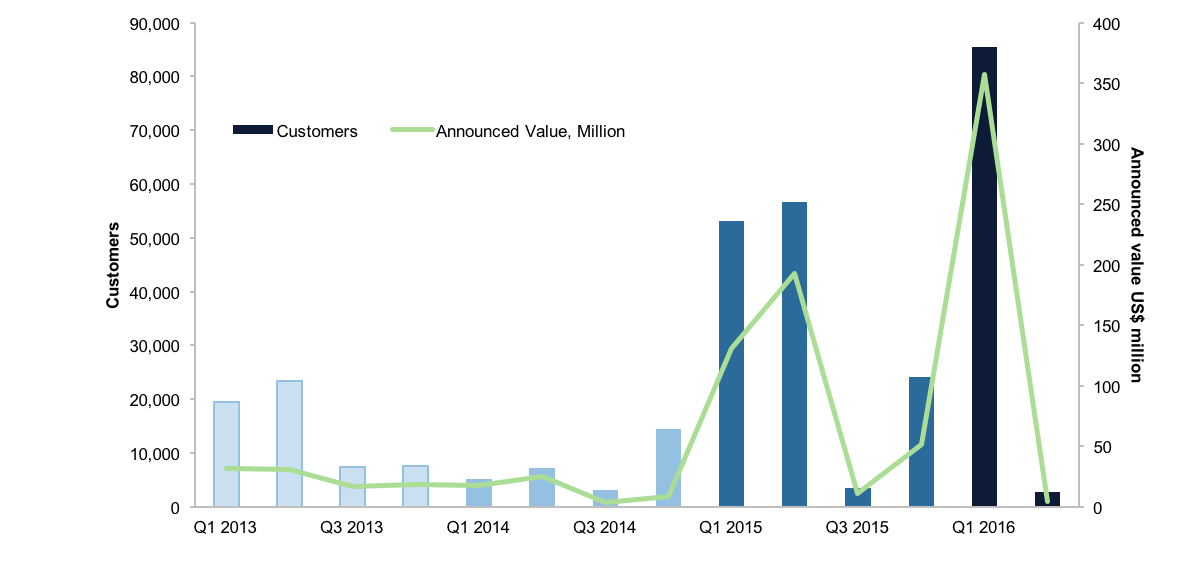

Exhibit: Investor-Owned Utility M&A (Q1 2013-Q1 2016)

Private ownership of a highly fragmented network of 49,000 systems represents 15% of the current market, but recent M&A activity signals a larger role for investor-owned utilities going forward. While American Water and Aqua America have been the most aggressive investor-owned utilities, more than 19 deals totaling US$384 million (completed and pending) are on the books for the first half of this year. Public-private partnerships (PPP) beyond O&M contracts have been employed sparingly in the U.S., according to Bluefield’s analysis. But pending PPPs in California, Florida, Indiana, and Texas for desalination, water treatment, and wastewater reuse plants indicate more acceptance.

“Many of the hurdles to private participation, including public pushback, asset bankability and debt financing remain, however, the broader, national focus on infrastructure upgrades is opening the door to more private participation,” says Hays.

“There is no silver bullet to solving the infrastructure challenge. Stakeholders must deploy a range of solutions including alternative financing, operations management, and innovative technologies.”

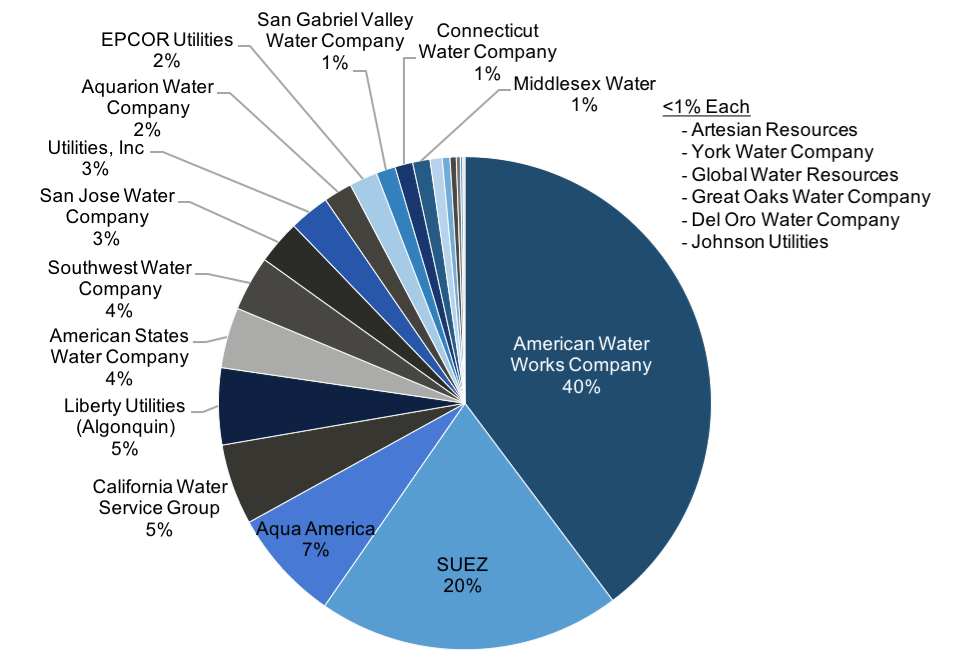

Exhibit: Large-Scale IOUs > 50,000 served

About the Report

These and other findings are found in Bluefield’s new report, U.S. Private Water Utilities: Market Trends, Strategies & Opportunities, 2016. This report provides strategic analysis of the top 25 investor-owned utilities, identifies key trends for private participation, and evaluates new opportunities for private players across state markets.

For more information or to speak to our water market experts please contact: Steph Aldock Marketing Director saldock@bluefieldresearch.com 415 404 8195